Credit card processing touches every modern sale, but the true cost of credit card processing is rarely obvious at first glance. Statements are dense, fee names change, and pricing models hide margins behind “simple” blended rates.

This guide breaks down the full picture in plain English for U.S. businesses. You’ll learn what drives fees, how to calculate your effective rate, how to compare providers, and how to reduce the total cost of credit card processing without harming approvals or customer experience.

If you accept cards online, in-store, or on mobile, the true cost of credit card processing is more than a swipe fee. It includes network assessments, interchange, processor markup, PCI and gateway costs, fraud tools, chargeback risk, and operational choices like terminal selection, settlement timing, and data quality.

By the end, you’ll know which levers you control, which are pass-through, and how to design a program that keeps acceptance high while keeping the true cost of credit card processing in check.

The Three-Layer Fee Stack That Determines Your Total Cost

When merchants evaluate the true cost of credit card processing, everything rests on a three-layer fee stack: interchange, card-brand assessments, and processor markup. Interchange is paid to the card-issuing banks.

Assessments are paid to the card brands for using their networks. Markup is what your processor or payment facilitator earns to provide services and support. Each layer behaves differently and shows up on your statement in different ways.

Interchange varies by card type (debit vs. credit vs. rewards), acceptance method (card present vs. card not present), and data quality (basic retail data vs. enhanced Level II/III for B2B).

Assessments are brand-set network fees that usually apply as small basis-point percentages or per-item amounts. Markup can be a flat percent, a per-transaction fee, a subscription, or a hybrid. Together, these factors determine the true cost of credit card processing on every sale.

To manage your total cost, you must separate pass-through items (interchange and assessments) from negotiable items (markup, gateway, ancillary tools).

Once you isolate markup, you can compare providers apples-to-apples and negotiate the portion of the true cost of credit card processing that you actually control.

Interchange: The Engine Room of Every Card Transaction

Interchange is the largest and most complex component of the true cost of credit card processing. It compensates the issuing bank for risk, rewards, and funding time. It is not set by your processor, and it changes based on transaction characteristics.

Card-present transactions at a countertop terminal generally qualify for lower interchange than card-not-present eCommerce transactions, because fraud and dispute risk is higher online.

Your MCC (merchant category code), average ticket, and the data you submit can shift your interchange outcomes. For B2B and B2G, providing Level II and Level III line-item details can help certain corporate or purchasing card transactions qualify for lower rates.

For debit, routing and regulation can influence costs and options. Although interchange is a pass-through, your operations—how you accept, what data you include, and how consistently you settle—can materially impact the true cost of credit card processing tied to interchange.

Understanding interchange tables can feel intimidating. Start with your largest transaction types, identify which interchange categories they fall into, and ask your provider to map volumes by category for the last three months.

This visibility reveals where optimization could lower your true cost of credit card processing without changing prices that you can’t control.

Card-Brand Assessments: Small Percentages That Add Up

Assessments are network fees collected by the card brands for using their rails. While each fee is small, the cumulative effect across your monthly volume can be meaningful in the true cost of credit card processing.

Assessments are typically charged as fractions of a percent plus small per-item or cross-border amounts. They are not the same as interchange, and they are generally non-negotiable because they are set by the brands.

For most U.S. merchants, assessments fluctuate predictably with volume and card mix. If you have heavy cross-border traffic, expect added network charges. If your sales skew toward premium rewards cards, the assessment’s impact may be incrementally higher.

The key is to ensure your processor passes them through transparently. When you review statements, verify assessments are itemized, not blended into a single “processing” line that obscures the true cost of credit card processing.

Because assessments are mostly fixed and brand-set, your strategy should focus on clarity. Transparent pass-through billing helps you confirm that assessments are charged as intended, preventing “quiet” margin creep that sometimes inflates the true cost of credit card processing.

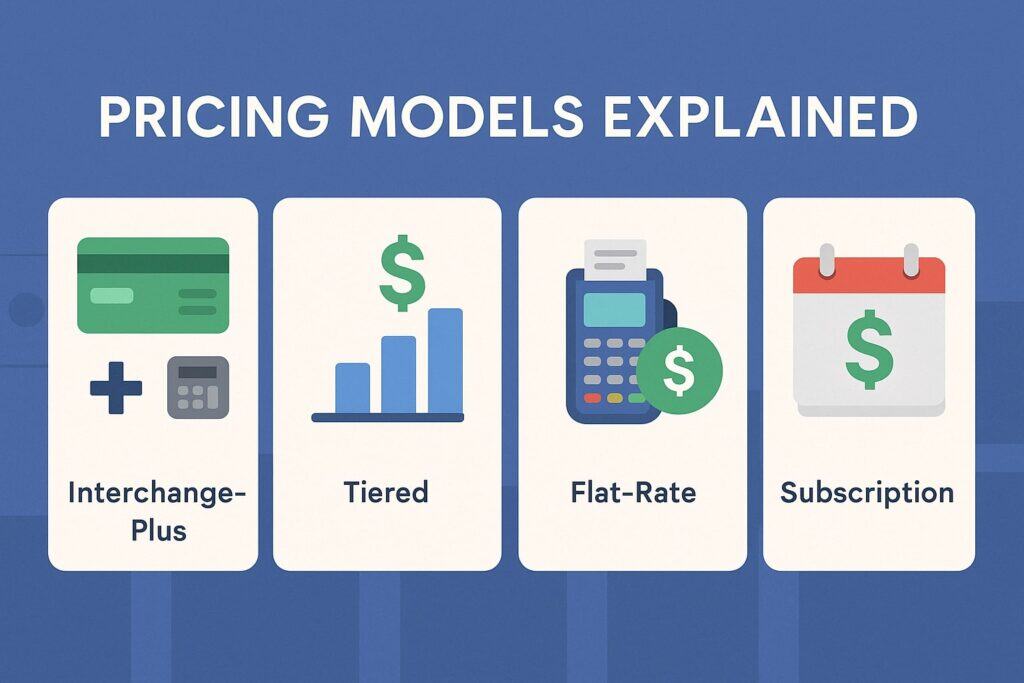

Pricing Models Explained: Interchange-Plus, Tiered, Flat-Rate, and Subscription

The pricing model you choose often determines how well you understand the true cost of credit card processing. Some models highlight real costs with a clear markup. Others mix pass-through costs with margins, making it difficult to compare quotes.

Your goal is alignment: a structure that matches your transaction mix and risk profile while keeping the true cost of credit card processing predictable and fair.

Interchange-plus (also called cost-plus) shows interchange and assessments as pass-through items and adds a stated markup (basis points and/or per-transaction). Tiered pricing groups transactions into “qualified,” “mid-qualified,” and “non-qualified,” which can hide markup variability.

Flat-rate pricing presents a single blended percent plus per-item, popular with micro-merchants and startups for simplicity. Subscription or membership pricing uses a monthly fee plus low passthrough-style per-transaction costs.

Choosing well means modeling each option using your actual card mix and average ticket. The same offer can be cheap for a $20 coffee shop but expensive for a $400 B2B sale. Always compute the effective rate so you see the real, all-in true cost of credit card processing.

Interchange-Plus: Transparent and Scalable

Interchange-plus is often the most transparent way to manage the true cost of credit card processing. You see interchange and assessments at cost, then pay a fixed markup—say, 10–25 basis points plus a per-item amount.

Because the markup is explicit, any future negotiation focuses on your provider’s earnings, not on opaque buckets or blended percentages.

Scalability is a major advantage. As your card mix changes or as you qualify for better interchange through data improvements (like Level II/III for B2B), the savings flow directly to you.

You also avoid surprises when brands adjust assessment structures, because those changes pass through at cost rather than being quietly absorbed into a higher blended rate that raises the true cost of credit card processing without explanation.

The trade-off is statement complexity. You’ll see more lines and more codes. But a good processor will give you category-level reporting and an interchange map so you can track drivers of the true cost of credit card processing. For most growing U.S. businesses, interchange-plus delivers the best balance of visibility and control.

Tiered, Flat-Rate, and Subscription: When “Simple” Costs More

Tiered pricing sounds easy—three buckets and you’re done—but it can lift the true cost of credit card processing because the provider chooses which transactions fall into “non-qualified.” That discretion often leads to higher margins on eCommerce, keyed, or premium-rewards transactions.

If you’re offered a “qualified rate,” ask to see what percent of your volume will actually qualify based on your last 90 days. That single question frequently exposes hidden costs.

Flat-rate pricing is predictable, making cash flow simple for small tickets and variable volumes. However, once your average ticket rises or your volume grows, a flat 2.6% – 2.9% type model may exceed the true cost of credit card processing achievable with interchange-plus.

Subscription pricing can work well for higher-volume merchants who prefer a fixed monthly fee plus near-cost transaction fees. The challenge is ensuring the per-transaction amounts and monthly fee pencil out given your ticket size and volume.

No matter the model, build a quick pro-forma using your last three months of data. The math will reveal whether “simple” secretly inflates the true cost of credit card processing for your exact business.

The Merchant’s Levers: What You Can Control (and What You Can’t)

To reduce the true cost of credit card processing, focus on the levers you control. You cannot set interchange or assessments, but you can affect how transactions qualify, how they route, which tools you use, and what markup you pay.

You also control operational policies that affect fraud, chargebacks, and PCI scope—each of which influences total cost over time.

Start with acceptance methods. Card-present EMV with chip-and-signature or chip-and-PIN typically costs less than keyed entries. Contactless (NFC) is treated like a card-present when properly captured.

For eCommerce, enabling 3-D Secure on risky segments can cut fraud and disputes and improve approvals, indirectly lowering the true cost of credit card processing by reducing loss and management time. For B2B, adding Level II/III data on corporate and purchasing cards can reduce interchange on qualifying transactions.

Finally, review your settlement and batching practices. Same-day, consistent batching minimizes downgrades for “late presentment.”

Small process fixes like AVS capture on keyed orders, CVV checks on eCommerce, and tokenized card-on-file frameworks reduce risk flags that would otherwise push transactions into higher-cost categories—raising the true cost of credit card processing.

Data Quality, Level II/III, and AVS/CVV Settings

Data quality is one of the most underrated levers affecting the true cost of credit card processing. Address Verification Service (AVS) and CVV results help issuers score risk.

Missing AVS on keyed or eCommerce transactions can trigger interchange downgrades and higher decline rates. Configure your gateway to require AVS for card-not-present and to reject obviously mismatched responses on high-risk orders.

For B2B, Level II data includes tax amount and customer codes. Level III adds line-item details like SKU, unit cost, and freight. Certain corporate or purchasing card transactions can qualify for improved interchange when you submit this detail.

Work with your gateway or ERP integrator to automate Level II/III population so staff doesn’t key it manually. Over time, this can meaningfully lower the true cost of credit card processing on your B2B mix.

Standardize settlement times, too. If your batch closes late relative to authorization, some transactions may not qualify for the best categories. A simple policy—batch every evening at a fixed hour—keeps your processing clean and protects the true cost of credit card processing from unnecessary downgrades.

Terminals, Gateways, and Tokenization Strategy

Hardware and software choices shape both risk and fees. EMV-capable, P2PE-validated terminals can remove sensitive data from your network, shrinking PCI scope and reducing compliance burden.

NFC contactless acceptance speeds lines and supports mobile wallets, improving approval rates and minimizing fallbacks to keyed entries that can raise the true cost of credit card processing.

In the gateway, turn on tokenization and vaulted credentials for card-on-file. Proper lifecycle management (account updater, network tokens) reduces declines on recurring or subscription charges.

Fewer retries and fewer customer contacts lower soft costs that rarely show on a statement but definitely raise the true cost of credit card processing when ignored.

Finally, avoid vendor lock-in where possible. Use platforms that support multiple processors or acquirers so you can benchmark pricing and performance annually. Optionality is leverage when you negotiate the components of the true cost of credit card processing you can actually influence.

Surcharging, Cash Discounting, and Compliance Considerations (U.S.)

Many U.S. merchants ask whether surcharging or cash discounting can offset the true cost of credit card processing. The answer depends on card-brand rules, disclosures, technical implementation, and state and local law.

Surcharging typically applies a fee to credit transactions; debit is generally excluded. Cash discounting reduces the displayed price for cash and offers a higher price for electronic payments if implemented correctly.

If you consider surcharging, verify card-brand requirements, signage, receipt language, and fee caps. Make sure your point-of-sale supports accurate fee applications only on eligible transactions.

For cash discounting, ensure you present a bona fide cash price and a non-cash price consistently, with clear signage. Misconfigured programs can lead to fines, customer complaints, or reclassification of fees, all of which increase the true cost of credit card processing.

Compliance extends beyond fees. PCI DSS applies to any merchant that stores, processes, or transmits cardholder data. Even with tokenization and P2PE, you must complete the correct SAQ (self-assessment questionnaire) and maintain policies.

Skipping PCI tasks may invite non-compliance fees and heightened risk, which indirectly raises the true cost of credit card processing through avoidable losses and penalties.

Practical Policy Tips That Keep You on the Right Side of the Rules

Create a written acceptance policy covering card-present procedures, eCommerce fraud checks, refund rules, and dispute handling. Train staff to avoid hand-keying unless necessary and to use fallback procedures properly.

Small improvements, like always inserting the chip rather than swiping or keying, reduce fraud and interchange downgrades, shrinking the true cost of credit card processing.

For eCommerce, deploy layered controls: AVS and CVV, velocity thresholds, device fingerprinting, and step-up authentication (like 3-D Secure) on risky orders. Document your fraud rules and review them quarterly.

As fraud patterns change seasonally, adjust tolerances so you protect revenue without adding false declines that hurt conversions and inflate the hidden true cost of credit card processing.

Finally, keep a “compliance calendar” listing PCI deadlines, policy reviews, and renewal dates for terminals and software. Proactive governance might not show up as a line item, but it prevents costly surprises that would otherwise inflate your total cost.

State Laws and Brand Requirements Change—Design for Flexibility

Because state laws and brand rules evolve, design your program to be adjustable. Use POS and gateway settings that let you enable or disable surcharging, dual pricing, or dynamic messaging with a simple configuration change.

Maintain template signage and receipt language you can update quickly. Flexibility minimizes downtime and retraining costs, keeping the true cost of credit card processing low even as the regulatory landscape shifts.

Work closely with your provider to receive advance notice when rules change. Ask for an executive summary of operational impacts and a checklist of action items. Treat changes like mini-projects—assign an owner, set a due date, and confirm completion.

This disciplined approach prevents rule changes from turning into fee surprises that bloat the true cost of credit card processing.

Chargebacks, Fraud, and the Hidden Costs Beyond the Statement

The visible fees on your statement are only part of the true cost of credit card processing. Chargebacks, representments, and fraud prevention tools carry direct expenses and indirect opportunity costs.

Every dispute requires staff time, documentation, and sometimes lost merchandise. Every fraud rule that’s too strict can reduce acceptance, creating false declines and lost sales that never appear on your processing invoice.

Start by tracking dispute reasons and win rates monthly. Identify patterns like friendly fraud on subscription renewals or shipment-related disputes for specific carriers. Optimize descriptors, use clear billing terms, and send proactive notifications for recurring charges.

Accurate tracking numbers and proof of delivery with signature on high-value orders help you win more representations, lowering the true cost of credit card processing associated with disputes.

Balance fraud controls with conversion. Tier your rules so low-risk orders flow through with basic checks while high-risk segments trigger step-up authentication. When you target friction where it matters, you preserve approvals on good orders and reduce wasted review time.

That balance reduces the hidden true cost of credit card processing—lost revenue and labor—while maintaining a friendly customer experience.

Building a Dispute-Ready Documentation Trail

The best chargeback defense is a clean paper trail. Use detailed order confirmations, shipment notices, and return policies presented before checkout. Store copies of AVS/CVV responses, IP addresses, device IDs, and delivery confirmations in a central system.

For point-of-sale, capture signatures only when required, but always maintain itemized receipts and refund logs. The more organized your records, the lower the operational true cost of credit card processing when a dispute arrives.

Automate evidence gathering where possible. Many gateways can package order details, invoices, and shipment data into a representation file. Set SLAs for your team—respond to disputes within days, not weeks.

Early, thorough responses improve win rates and shorten the lifecycle cost of each case, trimming the overall true cost of credit card processing tied to disputes.

False Declines: The Silent Margin Killer

Fraud filters that are too aggressive can decline good customers. False declines are expensive because they waste marketing spend and reduce lifetime value. Monitor approval rates by issuer, card type, and gateway rule.

If you see a dip, test changes like softening AVS strictness on low-risk baskets or enabling 3-D Secure to shift liability and boost issuer trust. Restoring approvals raises revenue without changing your posted price, lowering the effective true cost of credit card processing as a percent of sales.

Make testing ongoing. Seasonality, product launches, and promotional spikes all change your risk profile. A quarterly review of rules and outcomes ensures you’re not stuck with last year’s settings while today’s fraud looks different. This vigilance keeps your total cost aligned with reality.

Debit, Routing, and Least-Cost Strategies for U.S. Merchants

Debit behaves differently from credit in the U.S., and understanding your options can reduce the true cost of credit card processing. Card-present debit often carries lower interchange than credit, particularly for regulated debit issued by large banks.

Online debit may process on signature or PIN-less rails depending on your gateway and settings. Routing flexibility can influence cost and performance.

For in-store payments, ensure your terminals support multiple debit networks and proper routing logic. For eCommerce, ask your gateway about debit identification and routing capabilities. Some solutions dynamically choose the least-cost eligible network while maintaining approval performance.

Each incremental improvement helps bring down the true cost of credit card processing across high-debit mixes like grocery, quick-serve, and convenience.

Transparency is essential here, too. Request routing reports that show how many transactions took each network path and the resulting costs. If you see concentrations on higher-cost routes where alternatives exist, work with your provider to adjust configuration.

Over a year, small per-transaction savings accumulate into meaningful reductions in the true cost of credit card processing.

Average Ticket Size and Transaction Mix Matter

Your average ticket shapes whether debit optimization has a big payoff. Under $30, per-item fees loom larger; over $100, percentage markups drive cost. If your AOV is low, negotiate down per-item markups and look for debit routing that trims network per-transaction costs.

If your AOV is high, focus on basis-point markups and B2B data optimization. Aligning pricing with your mix prevents paying the wrong premium—and prevents accidental inflation of the true cost of credit card processing.

Be mindful of contactless and mobile wallets, too. They typically follow the same economics as card-present when captured properly, but they improve speed and reduce keying errors.

Higher throughput and fewer errors indirectly lower soft costs—labor time per sale and exception handling—which are part of the broader true cost of credit card processing even if they don’t appear on a fee line.

How to Read a Statement and Calculate Your Effective Rate

Every U.S. business should know its effective rate—the all-in percentage you paid for the month. Add all fees tied to processing (not equipment finance or separate software subscriptions) and divide by total processed volume.

That single number reveals your real, blended true cost of credit card processing, regardless of how many line items or pricing models are involved.

Break the total into buckets: interchange, assessments, and markup/tools. If your statement is interchange-plus, this is straightforward. If it’s tiered or flat-rate, ask your provider for a summary report showing pass-through vs. margin.

Scrutinize “miscellaneous,” “regulatory,” or “optimization” fees. Some are legitimate pass-throughs; others are simply markup with creative names that bloat the true cost of credit card processing.

Calculate the effective rate monthly and trend it across seasons. If it drifts up without a business reason (card mix shift, more CNP), investigate with your provider. Persistent increases often signal quiet margin creep or configuration issues that need attention to protect the true cost of credit card processing.

Spotting Junk Fees and Negotiating the Right Things

Watch for fees like “PCI non-compliance,” “inactivity,” “batch,” “monthly service,” “gateway access,” and “statement.” Some are reasonable; others can be reduced or waived. If you complete PCI tasks on time, non-compliance fees should never hit your bill.

If you use a modern gateway, “statement” or “regulatory” line items may be redundant or negotiable. Ask for a fee glossary and mark each item as pass-through, markup, or optional service. This clarity helps you lower the true cost of credit card processing quickly.

Negotiate markups, not interchange. Ask for tiered markups based on volume thresholds so your rate improves as you grow. If you process omnichannel, negotiate a single blended markup across in-store and eCommerce to keep accounting simple.

Lock in transparency—no rate increases without notice. These practical steps keep control of the portion of the true cost of credit card processing you can actually influence.

B2B Optimization, Recurring Payments, and Advanced Data Strategies

For B2B merchants, the true cost of credit card processing can drop substantially with data optimization. Many corporate and purchasing cards respond to Level II/III enhancements.

Integrating your ERP, invoicing, and gateway ensures tax, freight, and line items flow automatically. Consistent data improves interchange outcomes, reduces disputes, and accelerates cash application.

Recurring and subscription businesses should focus on tokenization, account updater, and intelligent retries. Use dunning emails with clear links and flexible payment dates to reduce involuntary churn.

For high-risk segments, step-up authentication or network tokens can boost approvals. Together, these tactics cut the soft and hard costs inside the true cost of credit card processing for recurring models.

Advanced merchants go further with network tokenization, card-on-file lifecycle signals, and BIN-level routing strategies. The payoff is fewer declines, fewer manual touches, and predictable costs.

Treat payments as a revenue discipline—not just a back-office function—and the true cost of credit card processing will fall as your acceptance and customer satisfaction rise.

Reconciling Faster and Closing the Books Cleanly

Accounting friction is a real component of the true cost of credit card processing. If payouts don’t match order batches, your team burns hours reconciling deposits, fees, and chargebacks.

Choose providers with detailed funding reports, settlement-date rollups, and export formats that match your GL. Align your batching time with your funding cutoffs so daily deposits match daily sales as closely as possible.

Automate as much as you can: deposit posting, fee accruals, and dispute reserve tracking. The fewer manual spreadsheets you maintain, the lower your hidden labor costs.

Clean reconciliation also tightens fraud detection—when numbers tie out, anomalies stand out quickly. Those early warnings help you stop issues before they become expensive, protecting the true cost of credit card processing from surprise losses.

Implementation Playbook: A 90-Day Plan to Lower Your Cost

A clear plan makes change manageable. In the first 30 days, gather data: last three months of statements, approval rates, dispute logs, and card mix. Compute your effective rate and separate pass-through from markup.

Capture current gateway settings for AVS, CVV, 3-D Secure, and debit routing. This baseline defines your current true cost of credit card processing.

Days 31–60, prioritize quick wins. Enable AVS/CVV requirements for card-not-present. Standardize batching. Activate tokenization and account updater for recurring. If B2B, turn on Level II/III.

Negotiate markup based on your baseline and secure written waivers for unnecessary monthly fees. Re-run the effective rate after these changes to measure impact on the true cost of credit card processing.

Days 61–90, optimize deeper. Pilot 3-D Secure on risky traffic, tune fraud rules to recover approvals, and evaluate hardware upgrades to certified EMV/NFC devices. Build a dispute evidence library and SLAs.

Set up monthly dashboards for approvals, chargebacks, and effective rate. With a feedback loop in place, you’ll continue shaving the true cost of credit card processing quarter after quarter.

What Good Looks Like at Steady State

In steady state, you’ll see transparent interchange-plus billing, stable or improving approval rates, predictable assessments, and a clearly stated markup. Fraud losses and chargeback ratios will trend down, while dispute win rates improve.

Your accounting team will reconcile daily with minimal manual work. Most importantly, your monthly effective rate will be steady or lower year over year—evidence that the true cost of credit card processing is under active management, not drifting upward unnoticed.

Keep a one-page payments scorecard: effective rate, approval rate, average ticket, dispute rate, and fraud loss per $1,000 processed. Review it monthly with your provider. A ten-minute meeting prevents a ten-thousand-dollar surprise and keeps your cost base honest.

FAQs

Q.1: What is the “effective rate,” and why does it matter?

Answer: Your effective rate is total processing fees divided by total processed volume for the period. It rolls every fee into one number so you can see the real, all-in true cost of credit card processing. Track it monthly to catch creeping costs.

Q.2: Is interchange negotiable?

Answer: No. Interchange is set by the card networks and paid to issuing banks. You can’t negotiate it, but you can influence which categories your transactions qualify for through data quality and acceptance methods—both of which affect the true cost of credit card processing.

Q.3: Which pricing model is best for most U.S. merchants?

Answer: Interchange-plus usually offers the most transparency and scalability for controlling the true cost of credit card processing. Flat-rate can be fine for small volumes or micro-tickets, while subscription/membership can work at higher volumes if the math checks out.

Q.4: How can I lower costs without hurting approvals?

Answer: Focus on data quality (AVS/CVV), EMV/NFC for in-store, Level II/III for B2B, and smart fraud controls with step-up authentication only on risky orders. These tactics reduce losses and downgrades while keeping conversions strong, trimming the true cost of credit card processing.

Q.5: Are surcharges or cash discounts legal everywhere?

Answer: Rules vary by state and card brand and can change. If you pursue these options, implement them with correct disclosures and technical controls. Missteps can generate fines and customer complaints that raise the true cost of credit card processing.

Q.6: What about debit routing?

Answer: Ensure your POS and gateway support routing across eligible debit networks. Least-cost eligible routing can reduce per-item expenses and lower the true cost of credit card processing, especially for low-ticket, high-debit merchants.

Q.7: Do PCI requirements really affect cost?

Answer: Yes. PCI compliance reduces breach risk and avoids non-compliance fees. Using tokenization and validated P2PE can shrink scope and effort. Skipping PCI often leads to fees and risk that inflate the true cost of credit card processing.

Q.8: Why do my approvals matter if I’m focused on fees?

Answer: Fees are only part of the equation. Lost approvals mean lost revenue. Improving approvals raises the denominator in your effective rate math, lowering the practical true cost of credit card processing as a percent of sales.

Conclusion

The true cost of credit card processing in the U.S. isn’t just a percentage on a brochure. It’s the sum of pass-through fees, provider markup, operational choices, fraud posture, routing, and data discipline. You can’t negotiate interchange, but you can shape how your transactions qualify.

You can’t eliminate assessments, but you can insist on transparent pass-through. Most importantly, you can align your pricing model, gateway settings, and hardware with your actual mix to keep the true cost of credit card processing low while maintaining great customer experience.

Make this a quarterly ritual. Calculate your effective rate, review approvals and disputes, and tune your setup. Negotiate markup with data, not anecdotes. Invest in tokenization, EMV/NFC, and Level II/III where they fit.

Over time, these practical steps compound into permanent savings—proof that managing the true cost of credit card processing is one of the highest-ROI activities a merchant can own.