Membership-based merchant pricing is a payment processing model where a business pays a fixed membership (or subscription) fee to access wholesale interchange and network costs, plus a small, transparent processor markup. Instead of paying a blended percentage on every sale, the merchant decouples its processing costs from sales volume.

The result is pricing that looks and feels like “cost” (interchange + assessments) with a flat, predictable access fee. For many US merchants—especially those with consistent volume, higher average tickets, or strong card-present sales—this model can reduce effective rates, simplify reconciliation, and encourage smart routing decisions.

Because membership-based merchant pricing emphasizes transparency, it helps owners understand exactly what portion of card fees are non-negotiable (set by the card networks) and what portion is processor markup (negotiable).

This guide explains how the model works, compares it with other pricing methods, shows when it fits best, walks through implementation, and answers practical questions about compliance, statements, ROI, and long-term scalability.

If you’ve ever wondered why your fees spike in busy months, or how to make interchange work for you rather than against you, membership-based merchant pricing offers a clear, modern framework that aligns processor incentives with your bottom line.

What Is Membership-Based Merchant Pricing?

At its core, membership-based merchant pricing separates access from usage. Rather than charging a percentage margin on every card sale, the processor charges a recurring membership fee that grants access to wholesale “pass-through” costs (interchange + card brand assessments) and a minimal, fixed per-transaction markup (often just a few cents).

Interchange is the fee paid to issuing banks; assessments are network fees paid to Visa, Mastercard, Discover, and American Express. Both are largely non-negotiable. Traditional plans bury a processor’s margin inside a blended rate, making it difficult to see how much is wholesale versus markup.

Membership-based merchant pricing flips that script. You keep interchange variability (which depends on card type, entry method, and data quality), but you remove the processor’s percentage spread. That means your effective rate often falls as ticket sizes grow, and your savings scale with volume.

Merchants appreciate that the membership fee is predictable, budgetable, and not tied to seasonality. This design aligns incentives: the processor earns the same membership revenue whether your card mix is premium or basic, so they focus on helping you qualify for the best interchange categories, optimize data, and reduce unnecessary downgrades.

In short, the model offers transparency, predictability, and potential savings—especially for businesses that value cost control and clean accounting.

How It Compares to Flat-Rate, Tiered, and Interchange-Plus Pricing

Flat-rate pricing is simple (e.g., 2.9% + 30¢) but can be expensive for larger or card-present merchants because it embeds healthy margins to cover all card types and risk profiles.

Tiered pricing groups interchange categories into “qualified,” “mid-qualified,” and “non-qualified,” often obscuring true costs and causing bill shock when transactions fall into higher tiers.

Interchange-plus is more transparent (interchange + assessments + a visible markup like 0.20% + 10¢), but the percentage markup still scales your fees as sales rise, and negotiating that percentage can be tricky.

Membership-based merchant pricing replaces ongoing percentage markups with a subscription fee and a tiny per-transaction add-on, enabling access to wholesale cost with minimal margin creep.

For businesses with higher average tickets or steady volume, removing the processor’s percentage spread can push the effective rate lower than flat-rate or tiered plans. For low-volume micro-merchants, a monthly fee may outweigh savings, making flat-rate simpler.

Interchange-plus remains a good middle ground for variable volumes or when a merchant is not ready for a membership commitment. The key differentiator is how processor margin scales: in membership-based merchant pricing, margin is essentially fixed, so more of your cost movement reflects genuine interchange shifts rather than opaque markup.

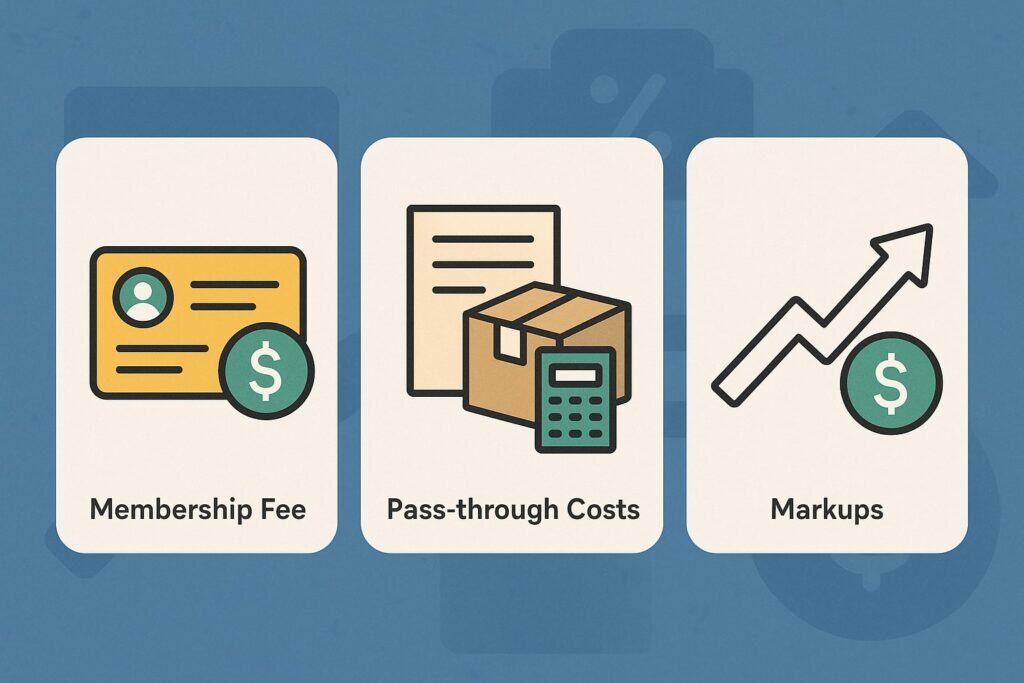

Core Components: Membership Fee, Pass-Through Costs, and Markups

Membership-based merchant pricing rests on three building blocks. First, a membership fee (monthly or annual) buys access to wholesale pricing. Tiers may exist—e.g., “Starter,” “Growth,” “Scale”—based on volume, risk, support level, and included software.

Second, pass-through costs (interchange and brand assessments) are charged at cost. Your statement should itemize these by card type and category (e.g., Visa CPS Retail, MC Merit I, key-entered, card-not-present).

Third, a minimal markup (often a per-transaction fee like 5¢–10¢) covers gateway or processing overhead that isn’t in the subscription.

Some providers add optional tools—like chargeback management, Level II/III data optimization, or network tokenization—either included or à la carte. Critically, there should be no percentage-based processor margin on top of interchange.

You’ll still see variability month to month because card mix and entry method drive interchange, but your processor take remains stable.

To evaluate offers, ask for a sample statement showing how the line items appear, whether the per-transaction fee is flat across channels, how PCI compliance fees are handled, and whether support, reporting, and terminals are bundled or billed separately. A clean membership plan lists every charge transparently so accounting can tie costs back to activity without detective work.

Who Benefits Most: Ideal Merchant Profiles in the US

Membership-based merchant pricing tends to shine for established US businesses with one or more of these traits:

(1) Consistent monthly volume (e.g., $50,000+), so the membership fee is diluted across many transactions;

(2) Higher average tickets (e.g., professional services, medical, B2B, specialty retail), where removing a percentage markup saves more;

(3) Card-present or EMV-heavy mix, where interchange can be relatively lower than card-not-present, further enhancing savings;

(4) Multiple locations or franchises, where a single negotiated membership tier can standardize costs and auditing;

(5) B2B or invoice-driven workflows, where Level II/III data can qualify for better interchange and the membership model puts the focus on data quality rather than margin.

Startups and seasonal micro-merchants might prefer flat-rate until volume stabilizes. High-risk verticals may face additional membership pricing constraints or reserves regardless of model.

Nonprofits sometimes do well under membership plans because donor card mix often includes rewards and corporate cards; pass-through transparency helps boards and auditors see exactly where fees go.

Ultimately, the fit depends on your volume, risk, sales channels, and appetite for transparency. If your effective rate under a blended plan has hovered above ~2.6% for in-store sales or ~3.0% for online, a membership plan is often worth a serious look.

Cost Modeling: How to Forecast Savings and Effective Rates

To size the opportunity, build a simple model: Total Cost = Interchange + Assessments + (Per-Txn Fee × Txn Count) + Membership Fee + Optional Tools.

Pull 3–6 months of current statements and extract: total card sales, transaction counts, average ticket, card-present vs. card-not-present mix, and the weighted average interchange from your existing plan (or estimate from itemized categories).

Next, simulate removing the processor percentage margin and replacing it with the membership fee plus the quoted per-transaction add-on. Keep interchange and brand assessments constant for the base case, then test scenarios with a better card-present mix, higher data quality, or address verification improvements to see impact.

Also test seasonality—in slower months, is the membership fee still justified? In busy months, how much does your effective rate fall when the processor’s percentage is gone?

Many merchants find breakeven around a predictable number of transactions: e.g., at 2,000 transactions per month, a $99 membership with 7¢ per-txn can beat a 2.75% + 10¢ flat-rate plan, especially as average tickets rise.

Be conservative: include edge costs like PCI, gateway, chargebacks, and any compliance tools. If you sell omnichannel, confirm whether the per-transaction markup differs between in-store and online. The final sanity check is cash cost per $100 in sales under each model—simple, board-friendly, and powerful.

Implementation: From Underwriting to Statements Without Surprises

Switching to membership-based merchant pricing starts with application and underwriting: ownership info, EIN, banking, processing history, and a quick review of products/services and fulfillment timelines.

Expect know-your-customer checks and, if your ticket size is high, a discussion of rolling reserves or funding delays (standard in payments). Next, choose your hardware and software stack: EMV/NFC terminals, a gateway or all-in-one platform, virtual terminal, recurring billing tools, and integrations with your POS, eCommerce cart, or ERP.

During boarding, ensure address verification, CVV, and postal code prompts are configured to help qualify transactions and reduce fraud. Ask your provider to enable Level II/III enrichment if you invoice corporations or government entities; this can materially reduce interchange.

Before going live, perform parallel testing on a few transactions to confirm statement line items and fee logic. After your first two cycles, reconcile statements against your model: validate that the membership fee is flat, the per-transaction fee is correct, and pass-through categories match the expected interchange tables.

Create a downgrade report (or ask your processor to supply one) to identify transactions that failed to qualify for the best categories so you can fix data hygiene or timing issues. With the right setup, the shift should feel seamless—except for the savings.

Compliance, Card-Network Rules, and Ethical Billing Practices

Membership-based merchant pricing doesn’t exempt you from card-network rules, PCI DSS responsibilities, or US consumer protection laws around disclosures and receipts. You must still display refund policies, honor acceptance marks appropriately, and follow rules for recurring billing (clear consent, easy cancellation, timely notifications on changes).

If you surcharge credit cards or run a dual-pricing/cash-discount program, ensure your approach aligns with state regulations and network requirements, including signage, caps, and parity rules between channels.

Separately, ensure your descriptor (the label on cardholder statements) is accurate and that support contact info is reachable. PCI compliance remains your responsibility, though many membership plans bundle PCI tools or SAQ guidance.

Finally, insist on clean statements: true pass-through interchange categories, itemized assessments, and a clearly labeled membership fee. Avoid “gotchas” like non-standard “program fees,” inflated network fees, or blended line items that hide margin.

Ethical billing is part of the value proposition; membership-based merchant pricing should reduce, not increase, ambiguity. Perform annual reviews, and keep a record of any add-on services you approve so accounting can reconcile increases to signed orders or contract amendments.

Risks, Trade-Offs, and When Membership May Not Fit

Every model has trade-offs. A membership fee introduces fixed cost—in slow months, your effective rate can temporarily rise. Card-not-present or high-risk merchants may not achieve dramatic savings because interchange remains elevated and risk controls add overhead.

If you run very low volume or micro-ticket transactions (e.g., sub-$10), a per-transaction markup—no matter how small—can weigh on costs relative to certain micropayments programs.

Statement simplicity depends on your provider’s discipline; if they tack on “program” or “regulatory” fees that aren’t true pass-through, you can lose transparency. Additionally, if your card mix is heavily premium rewards, pass-through interchange may still be costly; the membership model doesn’t change network economics.

Operationally, you’ll want a provider with strong chargeback tools, fraud screening, and support SLAs; savings aren’t helpful if you spend hours resolving disputes.

Finally, beware of contracts that pair membership with early termination fees or auto-renewal traps. Ask for month-to-month or a fair trial window. If a provider resists clear commitments on transparency, that’s a red flag—the whole point of membership-based merchant pricing is fewer surprises, not new ones.

Selecting a Provider: Questions, Negotiation, and Red Flags

Treat selection like a strategic vendor decision. Ask providers to (1) quote the membership fee, (2) disclose the per-transaction markup by channel, (3) confirm no percentage processor margin, and (4) share a sample statement.

Probe whether PCI, chargeback alerts, network tokenization, account updater, and Level II/III are included or billed separately. For omnichannel merchants, verify in-store, online, and keyed rates are consistent with the membership model.

Discuss funding times, reserves, and weekend/holiday settlements. During negotiation, focus on the total cost of ownership and support quality: hours, US-based support, named account managers, and resolution SLAs.

Red flags include blended line items labeled “compliance fee” or “program optimization” that scale with volume, vague “regulatory pass-throughs” that don’t match card-brand schedules, and restrictive cancellation clauses.

Look for clear living documents or knowledge bases that explain statement lines. A good membership-based merchant pricing partner welcomes audits, educates your team on interchange qualification, and proactively monitors downgrades so you keep more interchange-friendly behavior over time.

Technology Stack: Terminals, Gateways, and Data Quality

Your tech stack determines how well you qualify for favorable interchange and how much control you retain. For card-present environments, use EMV and NFC terminals with P2PE or strong end-to-end encryption; this reduces data compromise risk and supports contactless experiences.

For card-not-present, pick a gateway with flexible tokenization, stored profiles, recurring billing, and support for Network Tokens and Account Updater, which reduce declines and retries. If you invoice B2B customers, enable Level II/III fields (tax amount, customer code, PO number, item details) to unlock lower interchange bins.

Integrate with your POS, eCommerce, or ERP to automate data capture instead of relying on manual entry. Turn on AVS and CVV prompts to reduce fraud and improve qualification.

Use webhooks to sync settlement batches to accounting, and implement a routine reconciliation checklist: batch totals match deposits, fees match statement lines, and any retrieval requests are handled within deadlines.

Membership-based merchant pricing works best when the tooling is set up to minimize downgrades, route transactions efficiently, and surface exceptions quickly so your team can fix root causes instead of absorbing hidden costs.

Accounting, Reconciliation, and Tax Considerations

From an accounting perspective, membership-based merchant pricing makes cost allocation cleaner. Record the membership fee in a fixed monthly “processing subscription” expense account, while interchange and assessments flow through cost of sales or merchant fees with direct linkage to activity.

Because pass-through is itemized, finance can calculate a precise effective rate per location, channel, or product line. This helps with menu pricing, surcharge decisioning (where allowed), and contract negotiations with enterprise customers.

Reconciliation improves when statements align to batches and funding timelines, so configure payout reports to mirror bank deposits. For tax, merchant fees are typically deductible business expenses in the US; consult your CPA on categorization and any state-specific nuances.

If you also accept ACH or RTP, consider separate GL accounts to analyze card versus bank-rail economics. Finally, document your internal controls: who can change pricing, who approves new add-on services, how disputes are tracked, and how often statements are audited.

With the membership model, monthly audits are faster because fewer fee categories hide margin, allowing finance to spot anomalies and confirm the subscription continues to deliver ROI.

Measuring ROI: KPIs and Ongoing Optimization

Post-migration, track a simple KPI set: (1) Effective Rate (Total Fees ÷ Gross Card Sales), (2) Cost per $100 Sold, (3) Downgrade Rate (share of transactions missing target interchange categories), (4) Chargeback Ratio and outcomes, (5) Auth Approval Rate, and (6) Net Funding Time from batch close to deposit.

Compare these to your pre-membership baseline over at least three months to smooth seasonality. If your effective rate drops by 20–60 bps and your downgrade rate shrinks, the membership plan is working.

Review card mix: if premium rewards cards dominate, consider strategies like debit steering (where permitted and ethical), Pay by Bank, or ACH for invoices to diversify rails. Revisit your membership tier annually; as volume grows, you may qualify for lower per-transaction add-ons or bundled tools.

Share KPI dashboards with operations so frontline teams understand why capturing ZIP codes, invoice numbers, or tax amounts matters. Membership-based merchant pricing rewards operational excellence: better data equals better interchange, which equals lower costs—without relying on opaque processor spreads.

Future-Proofing: Trends That Complement Membership-Based Merchant Pricing

Several trends amplify the benefits of membership-based merchant pricing. Tokenization and lifecycle management reduce declines and re-processing fees, cutting waste at pass-through cost layers. Network updates that reward rich transaction data make Level II/III even more valuable for B2B merchants.

Alternative rails like account-to-account payments for invoices or high-ticket B2B help carve out transactions that are structurally expensive on cards. Destination-based sales tax complexity pushes merchants toward systems that reconcile fees and taxes cleanly—membership statements help auditors and controllers see through the noise.

SaaS-native POS and headless commerce architectures make it easier to embed the right gateway and routing, aligning with a pricing model that doesn’t penalize growth.

Finally, data-driven chargeback prevention (alerts, order insights) shortens dispute cycles, and when your processor margin isn’t percentage-based, both parties are incentivized to reduce absolute cost, not just shift it around.

In sum, as payments infrastructure evolves toward openness and transparency, a subscription-style access model fits the direction of travel—clear costs, measurable ROI, and fewer surprises.

FAQs

Q.1: What exactly is included in the membership fee, and what is still billed per transaction?

Answer: In a membership-based merchant pricing plan, the membership fee is the recurring charge that buys access to wholesale processing. Think of it like a “cost-plus pass” that removes the processor’s percentage markup.

What’s typically included: access to pass-through interchange and assessments, core gateway or processing access, baseline support, and often PCI tools or a compliance portal.

What’s not included—and still billed per transaction—are the actual pass-through costs (interchange and card-brand assessments) plus a small fixed per-transaction fee that covers platform overhead (often just a few cents).

Optional add-ons—such as Level II/III enablement, account updater, network tokenization, fraud screening, and chargeback assistance—may be bundled in higher membership tiers or priced à la carte.

The beauty of the model is transparency: your statement should separate wholesale costs, per-transaction markups, and the membership line. If you see additional “program” or “regulatory” charges that scale with sales volume, ask for documentation and card-brand references.

A clean membership plan keeps the subscription fixed, the per-transaction fee minimal, and everything else itemized so finance can reconcile quickly.

Q.2: How do I calculate my breakeven versus flat-rate or interchange-plus pricing?

Answer: Start by pulling three months of sales, fees, and transaction counts. Under your current plan, compute the effective rate (Total Fees ÷ Gross Card Sales).

Then simulate the membership model: add the proposed membership fee, multiply the per-transaction fee by your monthly transaction count, and keep interchange + assessments constant as pass-through. Compare totals to your current fees.

The breakeven occurs where Total Cost (membership model) equals Total Cost (current model). Sensitize for seasonality by running a slow-month and busy-month scenario. If your average ticket is high, removing a percentage markup typically shifts the breakeven dramatically in favor of membership.

If your volume is sporadic or tiny, the fixed fee may outweigh savings, at least until you grow. Many merchants also compute the cost per $100 sold under each scenario—it’s a simple way to present the decision to executives and franchisees.

Finally, test operational improvements (AVS, CVV, Level II/III) that improve interchange qualification; these benefits flow through in any cost-plus model and can be the difference between marginal and compelling savings.

Q.3: Does membership-based merchant pricing change my PCI or chargeback obligations?

Answer: No. Membership-based merchant pricing changes how you pay, not what you must do. You still need to complete the appropriate PCI DSS SAQ, maintain secure cardholder data practices, and adhere to dispute timelines and evidence requirements set by the card networks.

What can improve is your tooling: many membership providers include PCI portals, guided SAQs, and basic policy templates. Likewise, they may bundle chargeback dashboards, alerts, and representation services. Because the processor’s margin isn’t tied to your volume, they’re incentivized to help you reduce absolute costs—and chargebacks are costly.

Expect guidance on address verification, CVV, 3-D Secure for eCommerce, and consistent refund policies. Still, ultimate compliance rests with you. Make sure your terminals are EMV-capable, your eCommerce flows support SCA/step-ups where appropriate, and your staff understands how to capture data that qualifies for better interchange.

A membership plan makes statements clearer; it doesn’t remove the need for good security hygiene and timely dispute handling.

Q.4: Is membership-based merchant pricing good for card-not-present or subscription businesses?

Answer: It can be—especially if your average ticket is moderate-to-high and you invest in tokenization, account updater, and retries that respect issuer preferences. In card-not-present environments, interchange is inherently higher due to risk.

A membership plan removes the processor’s percentage spread, which can still produce savings, but your biggest wins will come from reducing declines, qualifying for the best CNP categories, and lowering fraud.

For subscription businesses, clearly disclose billing terms, send advance notices for changes, and make cancellation easy to stay compliant with consumer protection and card-network standards. Consider using network tokens to stabilize renewals and decrease re-entry of credentials.

If you also accept ACH for invoices or annual renewals, route appropriate customers to bank rails to diversify cost. Ultimately, the membership model aligns incentives around data quality and success rates—both of which matter more online—so if you’re prepared to optimize your stack, membership-based merchant pricing can be an excellent fit.

Q.5: What should I look for on my first statement after switching?

Answer: Your first statement is your truth serum. Verify that

(1) the membership fee is a single, flat line item

(2) processor margin appears only as the agreed per-transaction fee, not as a percentage anywhere

(3) interchange categories and brand assessments are itemized as pass-through with recognizable labels (e.g., Visa CPS, MC Merit, Discover DBI, Amex assessment)

(4) batch totals and deposits match your bank credits

(5) any optional services you approved are listed exactly as quoted.

Run a downgrade report to see if transactions missed ideal categories; fix root causes like missing AVS, key-entered card-present transactions, or delayed settlements. Compare your effective rate to the forecast you modeled and note differences explained by card mix or ticket changes.

If anything looks blended or ambiguous, ask your provider for a line-by-line reconciliation. Clean, auditable statements are a hallmark of membership-based merchant pricing; if the first month doesn’t match that promise, escalate early so the next cycle is rock-solid.

Conclusion

Membership-based merchant pricing reframes credit-card acceptance as infrastructure access rather than a variable tax on growth.

By paying a predictable subscription for wholesale access and keeping the processor’s margin fixed and minimal, US merchants gain cost clarity, easier budgeting, and a platform for operational improvements that actually show up in the numbers.

The model isn’t magic—it won’t eliminate interchange or assessments, and it won’t suit every micro-merchant—but for businesses with steady volume, higher tickets, or B2B invoicing, the economics can be compelling.

The shift encourages better data capture, disciplined reconciliation, and a proactive approach to downgrades and disputes. If your current plan obscures who gets paid and why, if your effective rate creeps up in busy months, or if you’re scaling across locations and need clean, auditable statements, membership-based merchant pricing is worth a thorough evaluation.

Build a simple model, request a transparent sample statement, and use your first 90 days to validate savings. When the processor’s incentives align with yours, payments become what they should be: a reliable, scalable utility that helps—not hinders—growth.