Buy Now Pay Later (BNPL) functions as a transformative power in digital payment systems, changing how consumers advance payments while transforming retail operations. As of 2025, Buy Now Pay Later solutions stand as the standard payment method among many consumers who expect to use this option, and the related transaction volume will reach $680 billion worldwide. Businesses seeking to implemention BNPL solutions need full knowledge about market conditions, benefits, implementation practices, and constraints to make informed decisions.

Understanding BNPL in 2025

As a short-term financial solution, BNPL enables purchasers to make their payments using installment plans for shopping without interest if they pay their bills on time. BNPL delivers unique features than standard credit cards since it performs compact credit reviews along with speedy point-of-sale authorization processes. The payment service directs remittances into four Sequential parts and prompts immediate payment at checkout, followed by subsequent fee-sized divisions over several weeks to months.

The Evolution of BNPL

The original special payment method transformed into an essential framework that now controls technological shopping operations. Traditional financial institutions and payment processors, nd technology-based giants added the BNPL concept after its initial adoption by fintech companies Affirm and Afterpay, and Klarna. Traditional banking entities teamed up with credit card organizations to develop BNPL products because they aim to challenge fintech leaders within the market by 2025. Payment processors maintain native BNPL functionalities on their platforms, while this service now operates across e-commerce stores and retail outlets, and service companies, together with business-to-business applications. Consumer debt-related concerns led to regulatory measures that established unique BNPL regulations to standardize the industry across various national regions.

Current BNPL Market Trends

Multiple vital developments will structure the BNPL market in 2025. Major mergers and acquisitions swept through the market, thus causing big organizations with complete solutions to decline in numbers. Strategic growth among BNPL providers came from developing financial systems that integrate banking services and shopping capabilities, with customer loyalty services. The implementation of advanced algorithms makes it possible for BNPL providers to boost their risk management systems by incorporating artificial intelligence for real-time credit decisions that show high accuracy. People utilize BNPL services for regularly scheduled payments or subscriptions to a greater extent than they do for individual purchases. Every retail sector sees increased customer purchasing amounts when businesses utilize BNPL solutions, according to available data.

Increased Conversion Rates and Sales

The implementation of BNPL solutions stands out as one major advantage because it drives exceptional conversion rate improvements. Research from 2024 demonstrates that businesses enabling BNPL gain more conversions, together with larger average order values and fewer cart abandonment events. The elimination of financial hurdles when making purchases at checkout becomes possible due to Buy Now Pay Later. Customers experiencing limited funds can achieve purchase completion through the ability to divide their payments into installments.

Customer Acquisition and Demographics

BNPL has successfully pulled in and retained groups of customers. People from Gen Z and Millennial demographic groups favor BNPL because they lack an extensive credit history or choose to stay away from traditional credit cards. Numerous providers indicate that new customers generate a substantial portion of BNPL transactions, which would not have occurred without this payment method. Evidence indicates that the growing number of consumers who use BNPL includes middle and higher-income customers who choose this method because of its convenience and improved cash flow abilities. By 20,25, BNPL transformed from its former demographics-based form into a standard payment solution that every consumer segment now expects to have access to.

Competitive Advantage and Market Positioning

Businesses in various sectors now use BNPL as a mandatory competitive tool instead of an optional advantage. Companies failing to provide BNPL payment solutions will inevitably lose their customers to businesses that enable flexible payments. The implementation of BNPL as a payment method allows customers to draw positive brand perceptions while creating collaboration potential with leading BNPL companies as well as access to new retail networks and enabling higher price points to target wider consumer bases.

Enhanced Customer Experience

Several factors support BNPL as an improvement factor for customer experience delivery. Understanding payment terms and fees becomes possible through the correct implementation of this concept because it displays payments clearly without extra costs. Quick approval processes allow shopping continuity, while extra payment methods let customers choose their preferred payment method. Research demonstrates that customers visit preferred payment method accepting merchants more often, which demonstrates how BNPL integration leads to better customer loyalty if done right through the buying process.

Challenges and Considerations

Financial Implications

Businesses that utilize BNPL solutions need to consider the complete financial aspects during their implementation stage. Borrowing providers demand payment from merchants as a portion of each purchased amount, whereas traditional payment methods require less expensive fees. Businesses building their pricing strategies in 2025 need to incorporate substantial fees from BNPL providers, even though elevated market competition has reduced the charges. The bulk of purchase funds from merchants reaches the merchant without delay, but providers work on distinct payment timelines that might impact cash flow management. Enhancing return management in BNPL transactions creates challenges for administrative staff who need to implement proper systems to control these processes effectively. Systems that handle accounting need proper configuration for unique aspects of BNPL payments because these payments might require enhancements in financial management processes.

Regulatory Landscape

BNPL now operates within a well-established regulatory framework by 2025. Major markets across the world adopted specialized BNPL legislation with consumer protection at its core, which businesses need to follow through with evolving standards. The implementation of BNPL solutions requires merchants, along with their BNPL partners, to support affordability evaluations while displaying absolute terms and fair dispute settlement methods. A successful BNPL solution requires organizations to verify that their system follows local regulations, even though rules differ between individual territories and may require specific modifications for each market. The importance of protecting customer data and respecting privacy stands high today because BNPL service providers acquire extensive consumer information, which creates legal exposure obstacles for merchants to understand.

Brand and Reputation Considerations

Businesses need to thoroughly measure the brand-related effects before making BNPL a payment option for customers. Luxury businesses need to evaluate their payment methods because BNPL has become popular, yet they must ensure options match their brand values alongside customer preferences. Consumer safety advocates warn that due to its design, BNPL might lead people to overspend among susceptible sector populations, thus putting linked merchants at risk of reputational damage. Vendor selection choice for BNPL providers directly influences missed payment management, which affects merchant brand relationships and customer brand perceptions.

Implementation Strategies

Selecting the Right BNPL Provider

In 2025, businesses must evaluate numerous BNPL service providers because selecting the right partner stands as an important strategic move. Provider recognition levels and user bases differ across markets, thus, geographic market suitability stands as an essential aspect. The technical compatibility between BNPL solutions and e-commerce platforms and Point of Sale systems directly affects both deployment timing and system implementation expenses. Evaluation of projected sales benefits requires comparison of commission rates and fixed fees, and minimum charges among different providers. How customers apply for BNPL solutions, alongside their experience with interface usability and approval rates, determines how customers will both interact with and feel about the service. Victorious retailers who currently present multiple BNPL options work toward increasing customer selection and approval rates through multi-provider strategies to generate additional selling potential.

Technical Integration Considerations

Implementation difficulties depend on the state of the business infrastructure and installed systems. Major e-commerce routes provide standard interface connections between their systems and well-known BNPL finance companies, which helps businesses streamline the launch process for typical applications. Organizations running custom e-commerce websites should examine API guides along with SDK availability and development assistance before choosing their payment provider solution. Companies need to plan systematically for delivering uniform access to BNPL solutions across both online channels and mobile as well as in-store points of sale to provide an exceptional omnichannel shopping journey. After launch, implementation testing must cover the full customer experience, especially edge scenarios, including partial refunds and order changes, to stop post-launch payment and customer service problems.

Marketing and Communication Strategies

The effective display of BNPL options plays a vital role in achieving high sales, along with satisfied customers. Appearing BNPL options from the beginning of shopping sessions instead of only during checkout improves consumers’ chances of making a purchase. Educational resources explaining both BNPL operations and benefits help consumers adopt this method, thus they remain valuable for increased usage. Product page display of installment pricing influences pre-checkout purchasing decisions, especially for expensive items. Rules of consistent service delivery for consumers require businesses in the retail sector to teach their staff about BNPL options. After a purchase, businesses must communicate payment plans properly to customers to stop payment failures, which generate damaging negative customer experiences that could harm brand reputation.

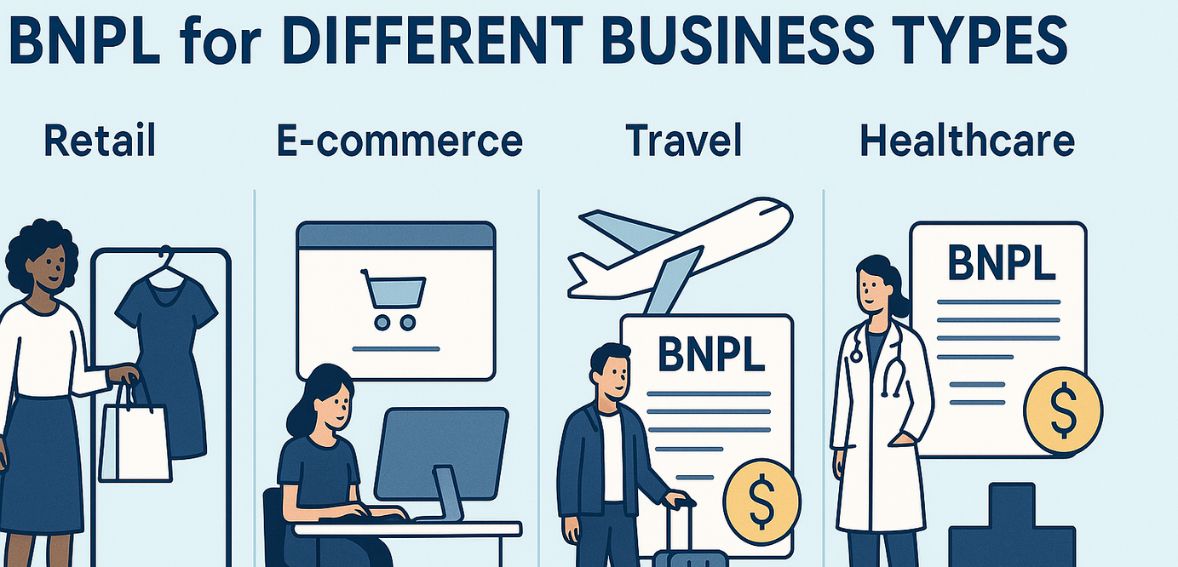

BNPL for Different Business Types

Retail and E-commerce

The retail sector stands as the main area where BNPL proves its value, especially through its effective deployment for fashion and apparel and electronics and technology and home furnishings and décor items and beauty and cosmetics products, and sporting goods products. The three sectors generate their greatest sales uplifts through BNPL since they focus on items valued between $100 and $1,000. Retail purchasing features where customers can easily see and instantly acquire desirable products through BNPL provide a perfect match for making premium items available immediately for extended payment terms.

Service Industries

BNPL has experienced substantial growth throughout the service sectors since 2025 while developing innovative financing possibilities for consumers. Medical facilities, together with dental and veterinary clinics, have started using BNPL payments to provide access to unreimbursed treatments, which enables patients to start treatment promptly opposed to delaying care due to monetary limitations. The integration of BNPL by airlines and hotels, together with travel agencies, allows customers to book trips during which they handle their money flow. Educational programs now use BNPL to enable students to pay their tuition fees and professional certification costs over time, which aids their professional growth. Home service providers who reconstruct and fix properties and manage substantial repairs benefit when clients receive flexible payment options that let them pay for essential building improvements without spending their life savings. The application of BNPL lets consumers pay for enhanced services that would cost beyond their means if not accessible through payment installments.

B2B Applications

B2B BNPL solutions have expanded extensively throughout different business sectors since 2025. Through inventory financing, smaller retailers can both stock products and extend installment-based payments to suppliers, which provides better financial control of supply chain cash flow. The accessibility to needed equipment improves through business procurement options that eliminate large financial prerequisites, hence enabling expansion possibilities for small and medium enterprises. Enterprise software and service vendors who enable subscription payments as installments encourage more businesses to adopt their technology solutions. Supply chain financing models based on BNPL principles optimize complex business financial efficiency through optimizing the flow of cash throughout their networks. The business-to-business applications utilizing the installment method consolidate payments across longer durations while supporting day-to-day operations, just like consumer BNPL. They process larger amounts at longer payment terms.

Measuring BNPL Performance

Key Performance Indicators

The assessment process for BNPL requires ongoing measurement of significant key performance indicators. The rate of adoption shows the extent to which customers opt for BNPL for their transactions. Firms can confirm their investment with provider charges and the cost of implementation through sales that happen solely due to BNPL availability. Firms can establish the basket size growth potential through average order value comparisons between BNPL payments and standard payment methods. Customer acquisition economics’ effect of BNPL enables companies to assess marketing effectiveness. Analysis of return patterns of BNPL purchases enables companies to forecast operational implications. Companies can quantify BNPL’s extended impact with customer retention and lifetime value metrics between existing customers and non-BNPL service users.

Data Analysis Best Practices

Advanced businesses use BNPL data to obtain more customer behavior and preference information. Businesses can create better promotion strategies once they understand which buyer segments favor BNPL products. The capacity to create profitable products through Buy Now Pay Later channels is employed to modify merchandise placement and promotion strategies. Determination of price points that yield maximum effect from BNPL gives organizations a method to increase product offerings and price systems. BNPL analysis enables more discovery of complementary products that offer greater cross-selling opportunities from the beginning of the purchase process to completion. BNPL analysis makes the payment method an instrument that offers strategic business insight, which directs marketing and merchandising efforts.

Future Outlook

The future of BNPL from 2025 will revolutionize the market through several forces that make BNPL a profitable business opportunity for merchants. The alliance of BNPL providers and merchants has developed programming that connects installment payments with loyalty programs to create an integrated system that supports repeat ordering. Decentralized finance processes based on blockchain technology build BNPL operations that eliminate costs while enhancing transparency, which leads to financial risks for traditional payment systems. The e-commerce buying system incorporates BNPL through internal integration, which makes BNPL operate as a background technical component. The integration of AI systems allows clients to select installment options based on their profiles and purchase history to support higher acceptance rates and handle risks effectively. The BNPL service providers proactively promote their solutions to offer sustainable buying solutions for durable goods to consumers willing to replace single-use products through sustainable consumption.

Conclusion

Businesses across all sectors will adopt BNPL as a basic payment method by 2025 in a bid to achieve some operational benefits. Many businesses that engage with consumers should consider adopting BNPL because it offers prospects of sales growth and broader customer bases, and easy shopping.

Companies must examine three critical factors to determine whether BNPL adoption is appropriate for their company: business context factors and customer demand, as well as monetary factors. Most companies have moved beyond the stage of BNPL adoption decisions to maximize immaximizeion of its usage and strategic selection of partnership providers.

Companies that want to reap the best from BNPL need to have ongoing awareness of industry trends and regularly review their strategies. Such exercises will help manage system complexities and costs. Entrepreneurial companies today view payment options as core business tools that create customer relationships while defining market presence and achieving competitive advantage in modern digital economies.